Tokenizing the World: The Potential and Challenges of Real-World Assets

Tokenization of real-world assets (RWAs) aims to bridge the gap between traditional finance and decentralized systems. From stablecoins and treasuries to real estate, commodities and luxury goods, tokenization of real-world assets promises to democratize access, streamline settlement processes, and disrupt traditional financial intermediaries. However, this paradigm shift is not without its challenges, as regulatory hurdles, liquidity concerns, and other barriers must be addressed. This comprehensive guide explores the current state of RWAs, their potential, challenges, and the implications for the future of finance.

Looking at the current state of RWAs

Stablecoins

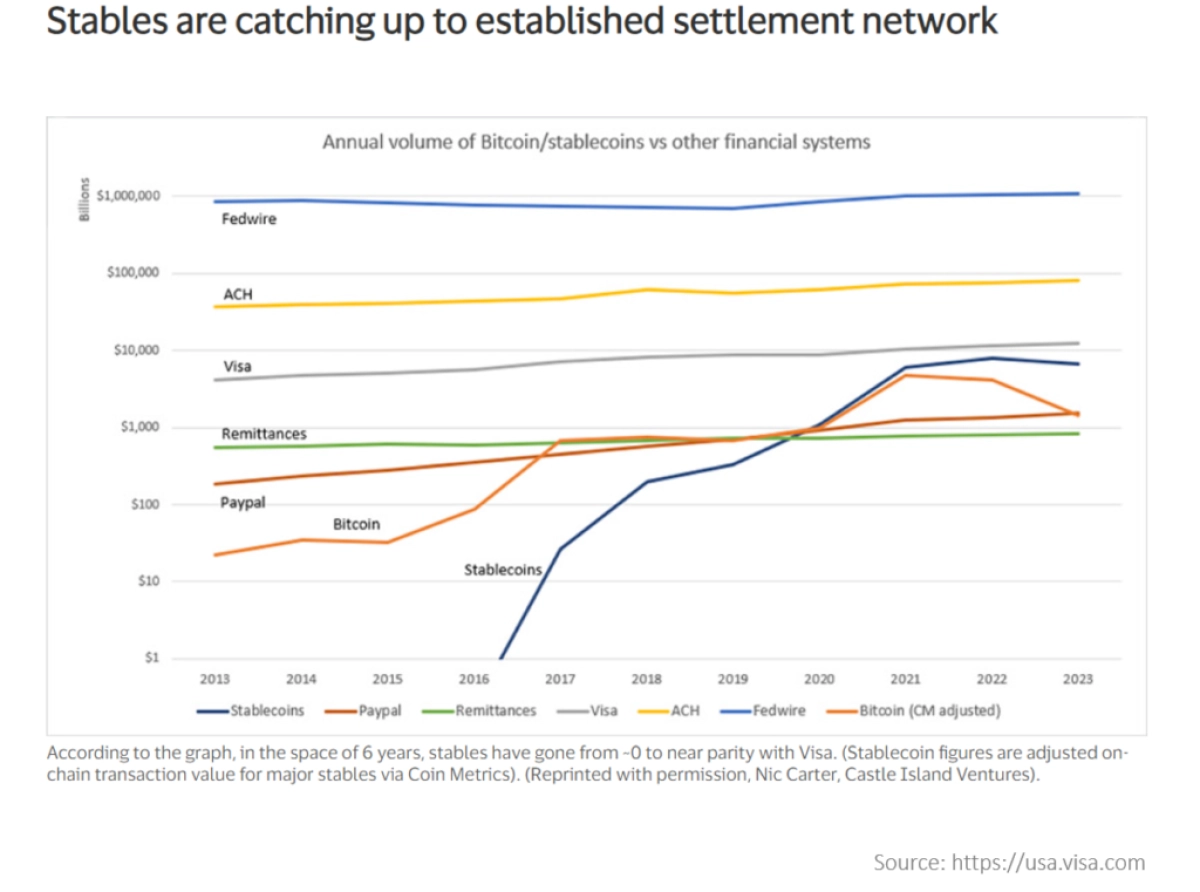

Among the various categories of real-world assets (RWAs), stablecoins have emerged as a massive success story. Stablecoin transaction volumes have caught up to and even started to surpass industry giants like Visa and PayPal. Recent numbers published by Visa indicate that last month’s stablecoin transaction volumes have exceeded Visa’s average monthly volume, a remarkable feat considering the long-standing dominance of traditional payment systems.

Source: Visa.com

While admittedly a significant portion of this volume can be attributed to trading bots rather than human transactions, the widespread adoption of stablecoins remains a testament to their product-market fit. Stablecoins have passed over the borders of the crypto ecosystem, finding practical applications in the real world, especially in developing nations.

In Argentina, for instance, individuals are increasingly turning to USD-backed stablecoins to preserve their purchasing power against the devaluation of the Argentinian Peso. In several African countries, USD stablecoins have become a widely accepted payment method, and internationally stablecoins facilitate seamless transactions across borders. Thus, Dollar backed stablecoins represent the first use case of Web3 finding real world adoption.

Besides currency-backed stablecoins, we also have commodity-backed stablecoins, pegged to precious metals like gold and silver or other commodities. Of the total stablecoin market capitalization they account for a mere 0.8%, with gold backed stablecoins making up 83% of their market cap. Due to their peg to a commodity instead of a currency, holding such coins is more akin to investing in the commodity rather than holding a stablecoin.

Tokenized Treasuries and yield bearing stablecoins

Stablecoins are mostly backed by U.S. treasuries, yielding around 5% for issuers like Circle and Tether creating a lucrative business model for issuers. Naturally users are now demanding a share of this pie. As a result, such yield-bearing stablecoins and dedicated tokenized T-Bill funds have been gaining traction.

As DeFi yields plummeted in 2023, tokenized treasuries experienced explosive growth, with users flocking to these instruments to gain exposure to rising U.S. T-bill rates. Providers like Ondo Finance, Franklin Templeton, and OpenEden witnessed massive inflows, as the total value locked (TVL) in tokenized treasuries surged by 782%, from $104 million in January 2023 to $917 million by year’s end.

Franklin Templeton’s fund is a retail instrument designed to provide access to T-Bills for investors who typically lack direct access to such products. Operating on the Solana and Polygon blockchains, the fund can only be purchased through the Franklin Templeton app, with no integration into the broader DeFi ecosystem.

In contrast, Ondo Finance’s products can be acquired on Ethereum, Solana, Mantle, and Sui. Its yield-bearing stablecoin USDY is backed by various investment vehicles, including BlackRock’s new BUIDL fund, BlackRock’s traditional T-Bill fund, and other U.S. treasuries and bank deposits. USDY is freely transferable 40 days after minting and is integrated within various DeFi protocols on compatible blockchains. Users who want USDY liquid immediately can acquire it on decentralized exchanges. While being a yield-bearing stablecoin, USDY is not pegged to $1. Similar to some liquid staking tokens, it the value of the T-Bill yield accrues to the token price. At the time of writing, one USDY is valued at $1.04. Mantle’s mUSD is a rebasing wrapped version of USDY, designed to maintain the peg at $1. The yield is therefore paid out to the user in the form of new tokens.

BlackRock recently entered the RWA space by launching their BUIDL T-Bill fund on Ethereum. BUIDL is not a tokenized version of an existing BlackRock fund, but an entirely new digital fund. With a minimum investment of $5 million and no DeFi integrations, it caters to institutional investors. On the surface it seemed to have an impressive launch, amassing $270 million within its first week. However, a closer look reveals that only a few large investors were responsible for the initial influx, including Ondo Finance which converted $95 million of its traditional BlackRock T-Bill Fund holdings into BUIDL.

A more crypto native approach to making US treasuries accessible to retail investors is Superstate, founded by Robert Leshner, the creator of Compound. Its T-Bill product currently has $86 million in assets under management. In the future, Superstate plans to expand its offerings and offer a wide variety of tokenized assets once this initial T-Bill product gains a firm foothold.

Private Credit

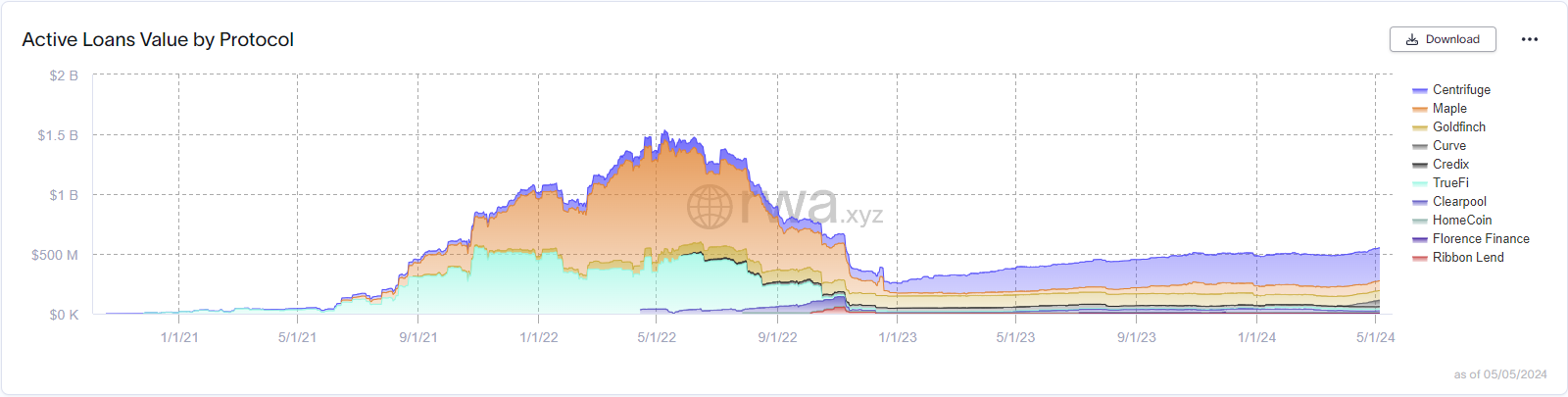

Another noteworthy segment within the RWA space are platforms that facilitate uncollateralized lending to private individuals and institutions based on their real-world credit scores. These platforms have found particular traction in emerging markets, where access to traditional credit channels may be limited.

During the previous bull market, private credit markets witnessed massive growth as speculative crypto funds sought uncollateralized loans to finance their activities. However, when market conditions turned bearish, the demand for such loans plummeted. The volumes are now gradually recovering, indicating a resilient interest in these alternative credit solutions.

Source: rwa.xyz

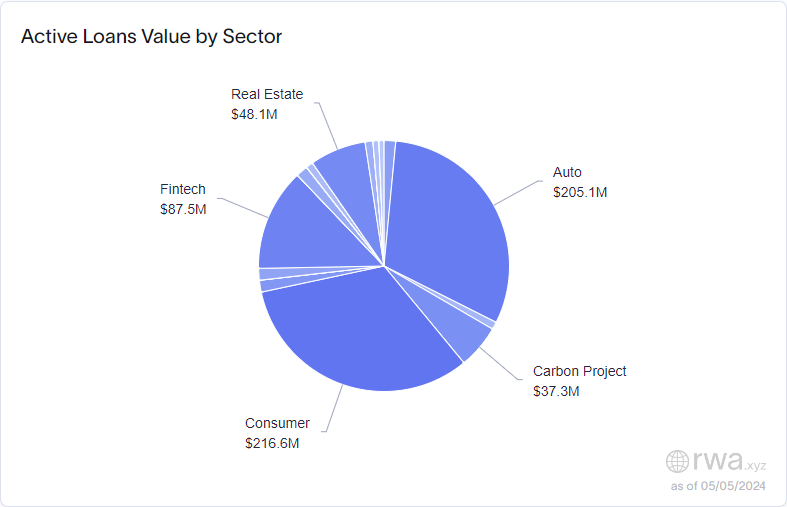

Private credit protocols cater to various sectors, with consumer and automotive loans being among the leading use cases. These platforms present themselves as alternatives to decentralized borrowing and lending protocols like Aave. While providing liquidity on such a platform is inherently riskier due to the lack of collateral, they provide the potential for higher yields, particularly during bear markets when yields on traditional DeFi platforms tend to be extremely low. As the crypto ecosystem continues to grow and attract a broader range of participants with varying risk appetites, platforms such as Centrifuge, Marble, and GoldFinch are well-positioned to gain further traction and increase their total value locked (TVL).

Source rwa.xyz

Real Estate and tokenized goods (Arts, Luxury goods, collectibles)

This is probably the RWA sector we see capturing the most attention on crypto Twitter. The focus is on tokenizing tangible assets and goods such as real estate, cars, expensive alcohol, or luxury goods like handbags. The idea is that the actual physical goods are stored securely, while ownership is represented by tokens that can be traded on-chain, aiming to give these assets money-like properties.

The promise is to enable improved liquidity and fractional ownership by bringing those assets on chain. For example, one could buy 10% of an office lot, without needing the capital required to purchase the whole property. They would then receive 10% of the revenue, while also having the ability to sell their tokenized shares at any time without needing to find someone willing and able to buy the entire lot.

However, the big problem currently facing these protocols is the lack of counterparties or market makers to provide sufficient liquidity for selling these tokenized assets. Without sufficient buyers and sellers, the liquidity for many of these assets is almost non-existent at this point.

Regenerative Finance

Another interesting domain within the RWA space is regenerative finance. Protocols building within this category aim to leverage blockchain technology to address environmental and social issues in the real world. This includes initiatives such as carbon credit trading, renewable energy markets, on-chain proofs of plastic removal from oceans, and public good funding mechanisms.

One of the key value propositions of using blockchains in this context is their ability to publicly verify the validity of assets. Traditional carbon credits for example face a long-standing issue, where many have been found to be ineffective or even fraudulent in offsetting the promised amount of CO2 emissions.

While a multitude of regenerative finance protocols are being developed or have already launched, none have yet achieved significant product-market fit or garnered massive attention. To turn such a project into a big success requires a lot of partners and organization. It necessitates the involvement of numerous non-governmental organizations (NGOs) on the ground to implement and monitor actual environmental projects. At the same time it also requires a wide range of buyers, primarily large traditional companies, to be willing to purchase these on-chain assets as part of their sustainability efforts.

Barriers to further adoption

Creating sufficiently deep liquidity

Achieving sufficient liquidity is the biggest obstacle to the widespread adoption of tokenized real-world assets. For an on-chain asset to be compelling, a liquid market with numerous potential buyers and sellers is essential. Without it, trading these tokenized assets becomes more challenging than transacting with the physical goods themselves.

To foster the demand necessary that sufficient liquidity can develop, the asset needs good integration within the DeFi ecosystem, providing additional utility compared to its physical counterpart. Stablecoins serve as a prime example for this. Being able to deploy capital within DeFi and earn yields, which a dollar in a bank account can’t. Due to this, USD stablecoins have garnered significant demand, resulting in a highly liquid market.

The lack of adoption of stablecoins backed by other currencies highlights how hard it is to get sufficient integration and liquidity. Despite the potential benefits for Europeans, such as mitigating taxation issues associated with using USD-based stablecoins, no EUR-backed stablecoin has achieved widespread adoption or integration within the DeFi space.

Lack of traction for many products

Although there should be value to tokenizing physical good RWA’s such as art, luxury goods, collectibles, and fashion articles, this segment has yet to achieve meaningful traction. Technically, tokenizing such items would make them easier to authenticate and transfer while fractionalization would make financial exposure to such items more attainable. However, perhaps the digital representation of such goods is too detached from the emotional value of owning and collecting them.

For example, an avid car enthusiast would absolutely love to own a classic Ferrari. Such cars have been great investments too and the real classics trade for millions. Although I may never afford one, I still personally would not consider buying into a tokenized Ferrari as it simply wouldn’t invoke the same emotional connection.

A 1962 Ferrari 250 GTO sold for $51.7 million. Source: https://robbreport.com/

Goods like expensive watches, classic cars, and high-end fashion typically derive their value from emotions and the satisfaction of collecting and owning those goods, not just financial appreciation. Tokenizing them and thus disconnecting from the emotion removes a large part of their value proposition. Thus tokenizing illiquid assets may not generate sufficient demand for enhanced liquidity, defeating the purpose of tokenization.

Other analysts may disagree, and there are cases where such assets have shown some traction. For example, ConstitutionDAO managed to raise nearly $47M in an attempt to acquire a rare copy of the US Constitution. There are other such efforts to tokenize luxury goods to make them more accessible and transferrable. However, it is likely that a more general adoption of digital assets is a prerequisite for any additional traction.

Regenerative finance products currently face similar issues as they struggle to find meaningful trading volume and liquidity. The core problem lies in the fact that these products are primarily tailored towards large traditional companies. These companies are far from operating on blockchains and will thus likely continue using traditional channels. This might change in a future where most financial transactions are settled on blockchains, but we are still a long way from such a reality.

Real estate RWA products seem to have better prospects. Real estate is less of an emotional investment – many people buy properties solely for investment purposes. Coupled with the fact that high prices prevent many from owning entire properties, products enabling fractional real estate investment with less capital could potentially find product-market fit. However, trading volumes remain relatively low, likely because only blockchain natives currently use these protocols. Like with private credit protocols, tokenized real estate should gain traction as the Web3 ecosystem onboards more users with different risk profiles than the classic crypto degen.

Challenges for institutions: privacy, fragmentation, and intermediation

As institutional players explore the tokenization of traditional assets, several key challenges emerge that need to be addressed for widespread adoption.

Privacy Concerns

On public blockchains, positions and holdings are visible to everyone, creating the risk of “stop hunting” – a practice where traders intentionally trigger others’ stop-loss orders. If stock trading moved on-chain, the exact positions of asset managers, banks and other financial institutions would be visible, creating a real risk that they would hunt each other’s stops by manipulating market movements. To mitigate this issue, institutions may require private blockchain networks.

Fragmentation Challenges

Currently, trading traditional assets across different companies, brokers, and intermediaries is complex and time consuming due to the fragmented system created by all these different entities. Tokenization in theory should resolve this issue by enabling seamless swaps with almost instant settlement. However, with multiple tokenization platforms built on various L1 and L2 blockchains, and some institutions potentially opting for private networks, Web3 has created its own fragmentation issues. Overcoming this challenge will require either industry-wide agreement on a few interoperable systems or the development of robust interoperability protocols.

Disintermediation Promises

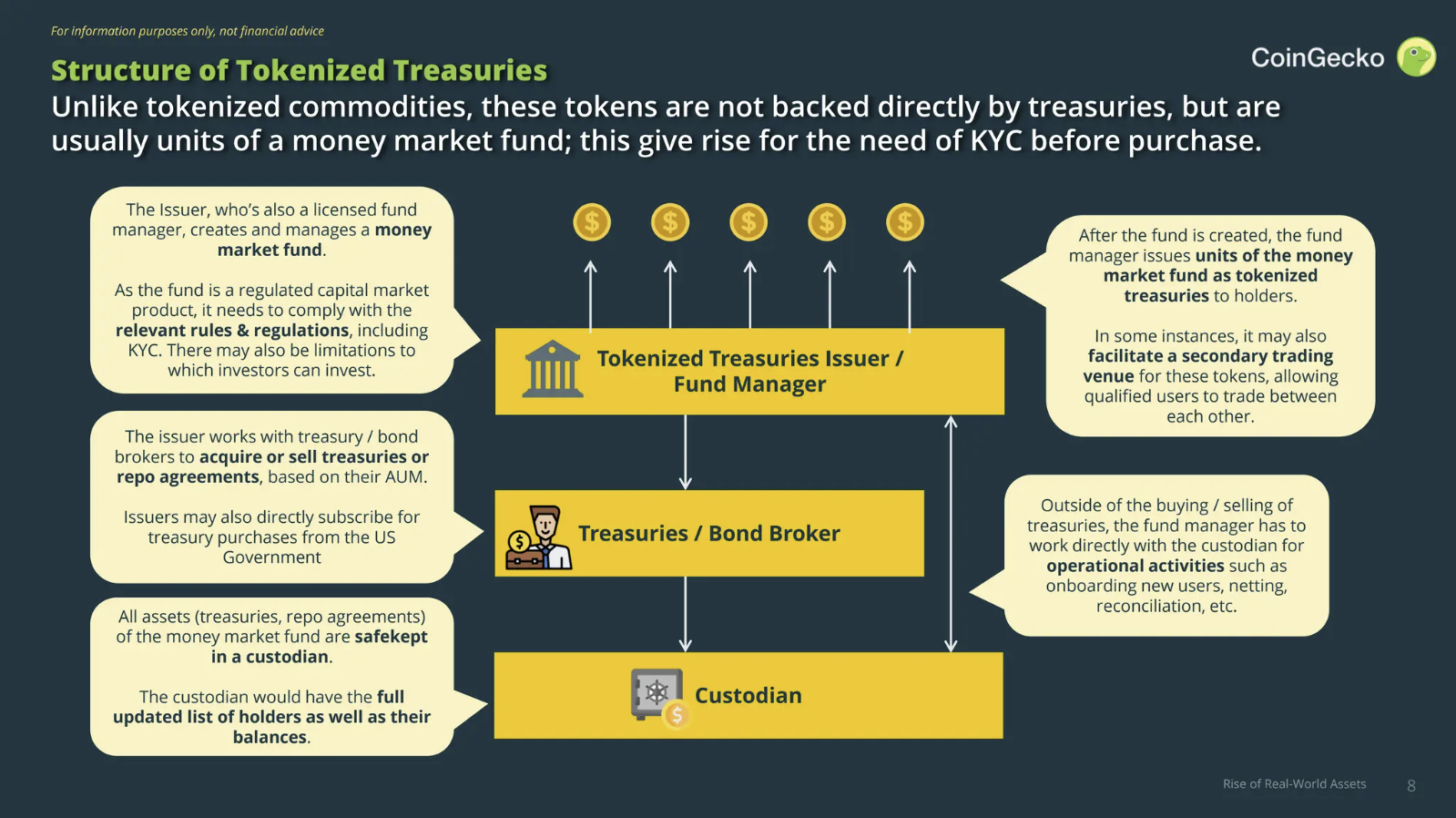

One of the touted benefits of tokenizing traditional assets is the potential to disintermediate the financial system. However, tokenized funds currently require a tokenization platform, placement agents, custodians, transfer agents, and investment platforms, resulting in a significant number of intermediaries. For instance, BlackRock’s BUIDL fund involves over half a dozen parties, including BlackRock Financial Management, Securitize, Coinbase, Anchorage Digital Bank, BNY Mellon, BitGo, Fireblocks, and PwC. Especially for securities under SEC jurisdiction, cutting out most intermediaries may be impossible due to legal requirements for investor protection. In order for tokenization to deliver on the promise of disintermediation, the process will need to be consolidated, automated and simplified.

Source: coingecko.com

Why are institutions bullish on tokenizing assets?

Considering all the challenges yet to overcome, and currently facing more drawbacks than benefits, the question arises: Why are Larry Fink and BlackRock such adamant proponents of tokenizing assets? Where do large institutions see the benefits in bringing traditional investment vehicles on-chain, especially for products like BUIDL that are institutionalized offerings not aimed at democratizing access?

The immediate benefits for institutions may appear limited, with the ability to trade 24/7 and achieve near-instant settlement being the most tangible advantages. However, Blackrock and their counterparts are playing the long game, recognizing the transformative potential of blockchain technology for the financial sector.

Once the challenges surrounding fragmentation, privacy, and regulatory compliance are addressed, moving trading onto blockchains could streamline operations, reduce costs, and enhance efficiency. By being early movers in this space, institutions like BlackRock aim to position themselves at the forefront of this technological revolution.

Moreover, the involvement of respected financial giants lends legitimacy to the tokenization of RWA and the blockchain industry in general, potentially facilitating regulatory progress. These institutions have a vested interest in transitioning the financial system onto blockchains, capitalizing on the theoretical benefits once the existing hurdles are overcome.

While the journey may be difficult, BlackRock and its peers seem convinced that tokenization will eventually reach escape velocity. Their current efforts are strategic moves to ensure they are well-positioned when that inflection point arrives.

Future Outlook on Real World Assets

Real-world assets can be divided into two distinct subclasses with very different implications: financial assets such as stablecoins, T-bills, private credits and securities on one hand, and tangible assets like cars, art, expensive whiskey and luxury goods on the other. Bringing financial assets on-chain makes a ton of sense, as exemplified by the massive success story of stablecoins, rising volumes of tokenized T-Bill and the biggest financial players pushing to tokenize the entire financial industry. The story is different for tangible assets. The benefit of bringing them on-chain, if they are to find sufficient demand and liquidity, will certainly require a wider adoption of blockchains by the general public.

Tokenized T-Bills appear to be the next big success story from the RWA sector. They represent the logical evolution of widely successful stablecoins. As we are seeing with USDe being integrated on exchanges as yield generating collateral, it will be even more logical for tokenized high grade RWA’s such as T-bills and other AAA type collateral to be accepted collateral as well.

On the institutional side there could still be a long road ahead until tokenized assets find the wide-spread adoption envisioned by proponents like Larry Fink and BlackRock. The reason lies in the simple fact that under current regulations, there is very little benefit from trading such assets on-chain. For non-blockchain-native organizations, instead of reducing friction, more friction is introduced. Regulatory changes tend to progress slowly and the largest capital market, the US, remains a challenging environment for the crypto industry. However, perhaps the regulatory landscape is improving. The SEC finally approved a BTC ETF this year, and just recently, the US House and Senate voted to strike down a SEC ruling that made it nearly impossible for financial institutions to custody digital assets. Meanwhile, Visa, Mastercard, JPMorgan, Citibank, Wells Fargo, Swift, TD Bank and others continue to experiment with a shared ledger to tokenize commercial bank money, wholesale central bank money, US Treasuries and other tokenized assets. It is exciting to envision a world where tokenized assets are used for instant settlement and clearing. The entire financial system would become more seamless and counterparty risk would be reduced.

The real-world asset sector is still in its very early stages. As it deals with assets present in the real world, this sector is subject to the most complex regulatory questions, which makes progress slow and tedious. However, stablecoins demonstrate that certain real-world assets can find amazing product-market fit when brought on-chain. The rising adoption of tokenized T-Bill products and private credits, as well as continuous large investments and support from important financial institutions indicate that more products outside of stablecoins may achieve widespread adoption in the future.

This article has been written and prepared by Lukasinho, a member of the GCR Research Team, a group of dedicated professionals with extensive knowledge and expertise in their field. Committed to staying current with industry developments and providing accurate and valuable information, GlobalCoinResearch.com is a trusted source for insightful news, research, and analysis.

Disclaimer: Investing carries with it inherent risks, including but not limited to technical, operational, and human errors, as well as platform failures. The content provided is purely for educational purposes and should not be considered as financial advice. The authors of this content are not professional or licensed financial advisors and the views expressed are their own and do not represent the opinions of any organization they may be affiliated with.

Leave a Reply

Latest News

More from GCR

Near AI x HZN – ...

We’re completing our coverage of Near Horizon’s first ever AI cohort and finishing off with a focus on decentralized compute. Previously, we highlighted the importance ...

Arweave’s AO Computer Has Big ...

Introduction Arweave has been a trailblazer in decentralized storage, providing an immutable data storage protocol on a blockchain-like structure known as the blockweave. The recent ...

Deep-Dive into Move-based Blockchains

I. Introduction Move is a new programming language for smart contract development. Originating from Facebook’s discontinued Diem and Novi projects, Move aims to revolutionize smart ...