A Detailed Study of the $AAVE Platform and Token

$GCR is a Tokenized Community of Researchers and Investors in the crypto space. Join our community today to get access to all the best investments ideas and deal flow, workshops and direct access to founders and key players in the space.

You will need 100 $GCR tokens to join the Discord community. You can purchase the token on Uniswap here and join the gated Discord group here.

Summary

Aave is a heavyweight in the DeFi lending space and has built the 3rd largest DeFi lending platform by TVL, as of this writing. With a strong liquidity ratio, healthy collateral spread and pioneering flash loans product, Aave is certainly making its mark in the space. However, with relatively high levels of collateral liquidation in the recent past, as well as high exposure of its flash loan business to the arbitrage use case, there are a few fundamental challenges that Aave faces in the immediate future.

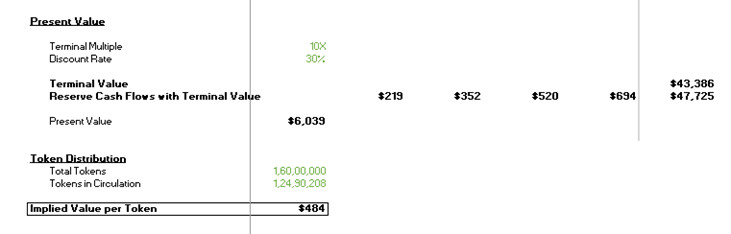

As for the $AAVE token, Aave has committed to using treasury reserves to buy and burn $AAVE tokens, which will decrease supply and could push up price. However, organic demand for Aave’s governance and security token $AAVE appears to be limited, with a ~22% staking rate. Based on our estimates of Aave’s treasury cash flow forecasts, we estimate the intrinsic value of the $AAVE token to be ~$484, with a high end of ~$856 and a low end of ~$135.

That said, the recently re-branded $AAVE is still relatively young, and the growth in adoption could surprise us. Overall, we will be keeping a close eye on this project as the story unfolds.

The complete model can be found here.

DeFi Overview

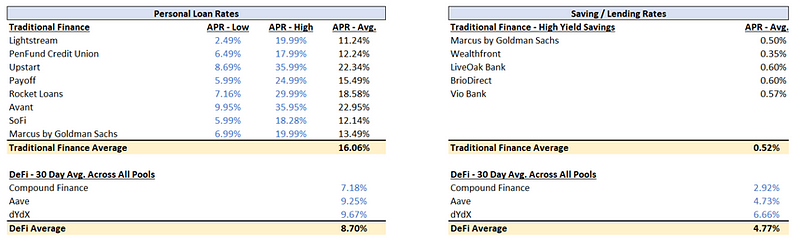

Lending platforms have been leading the DeFi ascent over the past year. Through these platforms, crypto holders can both avail loans with crypto collateral and deposit their crypto to earn interest. Depositors place their cryptocurrency in a lending pool and earn an attractive passive return on their crypto savings. Borrowers can borrow against their crypto, and loans are overcollateralized to protect against downside price volatility on the crypto collateral. This also allows loans to be of an indefinite period?—?borrowers can hold their loans for as long as their collateral remains above a certain amount.

Interest rates for lenders and borrowers are typically variable and determined by utilization of the deposit amount. This system protects all parties involved and eliminates the need for long process and third parties such as banks. By offering generally attractive rates on both sides of the transaction, it is no wonder that lending protocols are taking the world by storm.

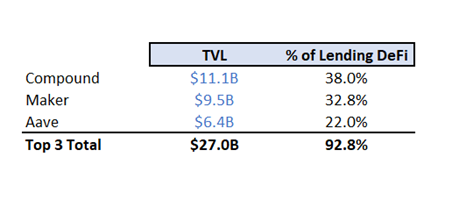

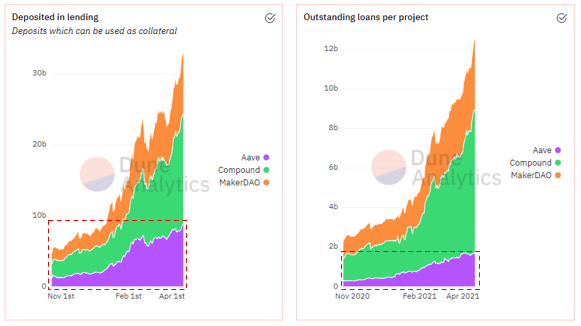

The lending DeFi space currently has $29.1B in total value locked (~50% of the $59B TVL in DeFi). Of this, Compound, Maker and Aave are the top players, capturing ~92% of the lending DeFi space.

Aave, one of the first DeFi lending platforms, originally launched in 2017 as EthLend, before re-branding to Aaave. Incremental to the traditional DeFi lending and borrowing products, Aave also offers Flash Loans (detailed below) and stable borrowing interest rates, which other platforms do not.

How does Aave Work

Aave has two key products: 1) traditional lending and borrowing, and 2) flash loans.

1. Traditional Lending and Borrowing

Like peers such as Compound and Maker, Aave’s core business is lending and borrowing platform. Aave currently supports >20 cryptocurrencies (such as ETH, DAI, USDT, USDC etc.) on its platform. This is how the process works: a depositor who, for example, deposits ETH will receive an aETH token in exchange. This token is interest baring, which means that when the depositor wants to withdraw their deposit, they can return the aETH and receive their original ETH plus the interest collected.

During the loan period, the ETH will be deposited in a pool from which borrowers can submit collateral in any other currency and borrow ETH. All loans are overcollateralized, which means the value of the collateral must be higher than the received value of the borrowed asset; borrowers can then choose between a fixed and variable interest rate. Loans are also of an indefinite period, which means that a borrower can hold the borrowed asset for as long as they like, provided the price of the collateralized asset remains above a certain level.

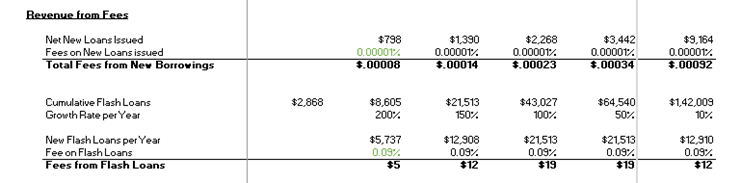

Aave keeps the spread and charges a 0.00001% fee on all loans at origin.

2. Flash loans

Flash loans are uncollateralized loans where the borrowing and repayment both occur within the same block. This is a product that was pioneered by Aave and ~$2.8B worth of flash loans have been completed on the Aave platform to date. There are currently three use cases for flash loans: 1) arbitrage, 2) collateral swap, 3) liquidation.

The arbitrage use case exists primarily because interest rates across lending platforms are not coordinated, allowing for some opportunity to users to profit from the spread. A flash loan ensures that assumption rates are locked in when making an arbitrage trade. The collateral swap and liquidation use cases exist primarily when the price of a borrower’s collateral is falling below the threshold level.

Both use cases allow the borrower to cap their losses at a fixed price higher than the official liquidation price. Aave currently charges a fixed 0.09% fee per flash loan transaction.

Evaluating the Aave Platform

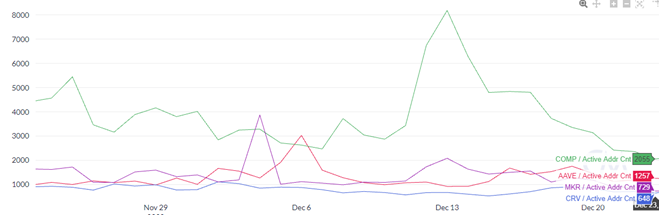

Utilization and active users is one of the first fundamental factors we looked at. When it comes to daily active accounts, Aave currently trails only Compound, with Maker and Curve close behind.

Given that Aave has reasonable user engagement, we then turned to the fiscal metrics that might indicate the health of Aave’s lending business. To assess this we looked at three metrics: 1) loans outstanding / total deposits and 2) distribution and relative strength of collateralized assets and 3) historical liquidation rate.

1. Overall, Aave performs better when it comes to liquidity management. With a similar deposit rate as Maker, Aave has fewer loans outstanding. This is a positive sign in a market when loan durations can be infinite and acceptance of high interest rates when utilization increases can break the system.

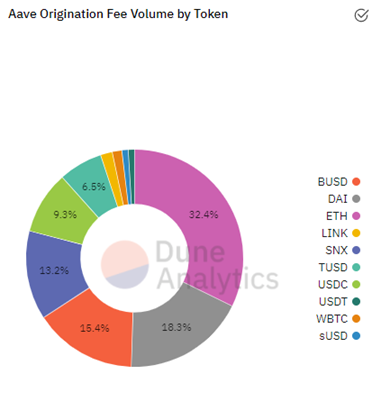

2. Based on the split of origination fees, a majority of the collateral on Aave’s platform is in blue chip, relatively stable assets such as DAI, BUSD and ETH. This is also a positive sign for the stability of the platform?—?if collateral were skewed towards smaller, more volatile assets, short periods of poor market breadth could trigger a large number of liquidation events, which could destabilize the platform.

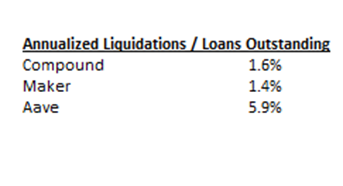

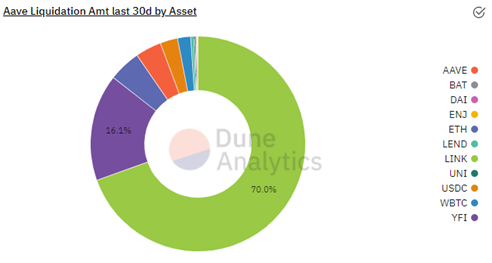

3. The one fundamental yellow flag for Aave is that its annualized liquidations, based on this past month exceed that of other lending platforms.

A large part of this was attributable to liquidations in LINK, which makes up a small share of Aave’s collateral pool. If this was a one off event, the warning signs could be turned off; however, if this sustains it could cause some instability in Aave’s platform.

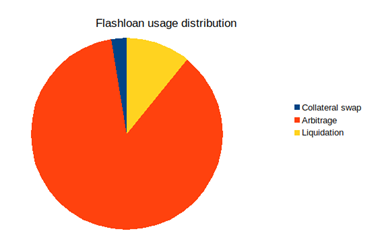

Finally, we took a look under the hood of one of Aave’s most unique product: flash loans. Namely, we wanted to understand whether the volumes that they are currently doing are sustainable. Based on the data we found, >80% of flash loans are currently being used for arbitrage. This is another yellow flag, given that as information asymmetry declines, arbitrage opportunities will begin to disappear across the DeFi landscape. If there aren’t any other meaningful uses of flash loans by that time, this could be problematic for this particular revenue stream for Aave.

Overall, Aave is one of a handful of large players operating in a rapidly growing market. Outside of some risks around liquidation, the health of the platform appears stable by most measures. What is important to remember with most of these protocols is that the interaction between platform and token varies depending on the protocol. Therefore it will be important to evaluate the tokenomics of the $AAVE token to understand its true value from an investment point of view.

Tokenomics

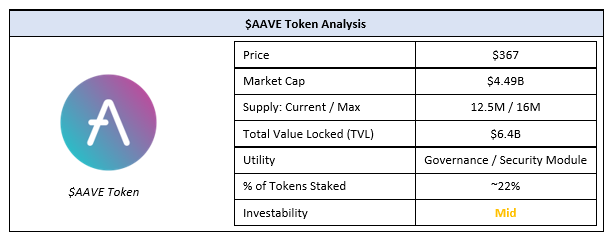

There are a total of 16M $AAVE tokens, of which ~12.5M are currently in supply, with he remaining 3M owned by the founding team. This level of decentralization is certainly encouraging when compared with Compound, where ~50% of tokens are still owned by the founding team and investors.

The $AAVE token has two key use cases: 1) governance and 2) securing the protocol. The governance use case is relatively straight forward. Holders who stake the coin get to participate in the operating decisions of the platform. The second use case goes as follows.

Holders who stake the coin can participate in the security module and earn a yield of ~7%. In exchange, their staked $AAVE tokens could be slashed up to 30% in the event of a liquidity crisis for the protocol.

This system is relatively new and Aave hasn’t gone through a liquidity crisis since the security module was announced. This makes it difficult to assess the likelihood of such events and therefore the attractiveness of the proposition. That said, this use case is certainly more attractive than the governance-only propositions of platforms such as Compound.

Currently, only ~22% of $AAVE token holders stake their token. This is in comparison to ~49% on peers such as Curve DAO. This is an indicator that the organic demand for the $AAVE token may not be as strong as we would like it to be.

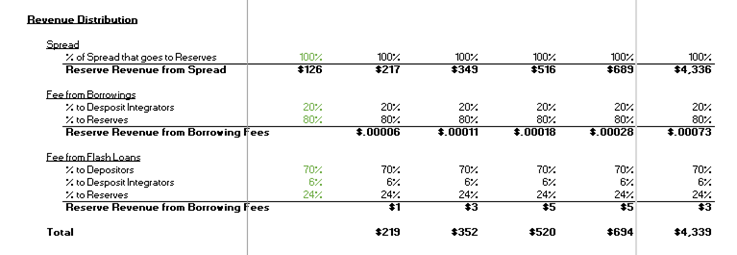

As with most platforms, Aave has a treasury where a portion of the spread earned from lending and borrowing and fees from flash loans are deposited. The current purpose of this fund, in Aave’s case, is to buy more tokens on the open market and burn them. This will add deflationary pressure on supply, and potentially upward pressure on price, by partially offset the lackluster organic demand.

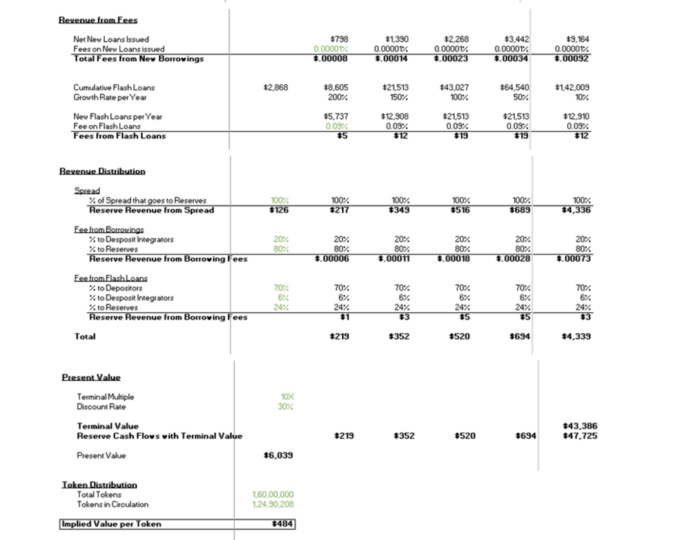

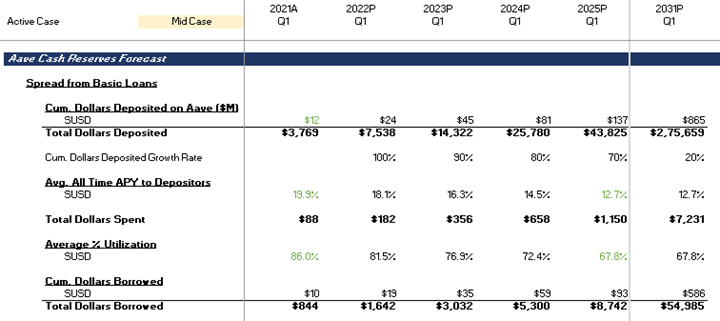

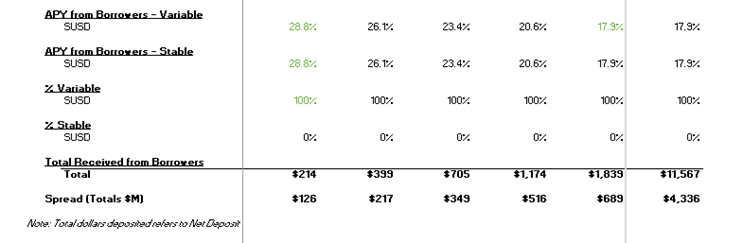

In the future, as with many other DeFi protocols, treasury cash flows could also be distributed as dividends to shareholders, based on a governance vote. To estimate the intrinsic value of the $AAVE token, we calculated the present value of forecasted cash flows to the treasury and divided it by the number of tokens in distribution.

Methodology

1. Begin with current deposits, utilization, recent interest rates (borrowing and lending) and flash loan data from Aaave’s AaveWatch dashboard

2. Create bookends for the increase in future deposits, based on historical trends

3. Assume that utilization, lending APY and borrowing APY mean revert towards historical all-time figures over time and remain at those levels in the long run as demand and supply balance

4. Calculate borrowings based on utilization

5. Calculate the spread earned from lending and borrowing over time?—?this is the largest cash flow generator for the platform

6. Create bookends for the growth of Flash Loans, based on historical figures

7. Calculate fees on borrowings and flash loans that are attributable to Aave’s treasury

Results

Assuming that the entire value of the spread every year is deposited in the treasury and growth rates for deposits and flash loans remain aggressive over the coming years, we found that the estimated intrinsic value of the $AAVE token is ~$484, with a high end of $856 and a low end of $135, based on their cash flows.

Eventually, however, a token’s price is based on the demand and supply for that token. In the case of $AAVE, the fact that reserves are being used to burn supply is a positive sign for price action. However, at the moment, with 22% staking the organic demand (outside of demand from speculators) does not seem as strong. This is likely in part because investors need to better understand the risk / reward of staking tokens in the Security Module; given its short history it may take a few market cycles to understand the likelihood of a liquidation event. Additionally, the ~7% yield might be a relatively week pull altogether, given that several other protocols such as Yearn Finance are able to offer much higher yield-based returns.

Over time, if token holders and investors begin seeing value in Aave governance and / or yield from the security module, we might see more staking, which would be a positive sign for organic demand. Until then, it may be best to invest in $AAVE purely based on price action, in order to get short term exposure to the lending DeFi space.

A brief look at the results from our model:

The complete model can be found here.

Leave a Reply

Latest News

More from GCR

Featured GCR Announcement GCR Exclusive GCR Quarterly Review

GCR Market and Investment Trends ...

By Global Coin Research Team Highlights GCR is a research and investment community. As a collective, we source investments, conduct research and diligence, and make ...

The Landscape of Crypto Intents

Introduction The current blockchain paradigm requires users to devise a specific series of transactions to achieve a desired outcome. However, crafting transactions can be complicated. ...

Near AI x HZN – ...

In our last article, we outlined Near’s vision to become the hub for User-Owned AI and the steps that it is taking to develop an ...