What Drives High DeFi Yields and What This Means for the Future of DeFi

Introduction

DeFi has become one of the pillars of the digital ecosystem, and is widely touted as one of the key disruptors coming out of the digital assets space. In many cases, DeFi has become an auto-response for anyone explaining crypto use cases to no-coiners.

As of this writing, DeFi (on Ethereum alone) has ~$63B in total value locked (TVL), which is substantial by most measures. With yields ranging from 15% all the way up to 1,000%+ on newer protocols, lending DeFi has become the base for several offshoot business such as automated yield aggregation. So it’s no wonder that DeFi has been the talk of the town. However, this does posit the question: what is driving the demand for lending DeFi, and the broader DeFi ecosystem by extension? And who is taking loans at these exorbitant prices?

How Lending DeFi Works

Let’s first start with a high level understanding of how lending protocols work.

- Borrowers can post crypto collateral and avail an indefinite-term loan, so long as the collateral value remains within range

- All loans are overcollateralized in order ensure loan security, given the volatile nature of the underlying collateral

- Borrowers must pay back these loans with interest whenever they wish to reclaim their collateral

- Lenders can pledge their crypto assets to provide liquidity to the protocol, and earn an interest in return

- Interest rates are auto-determined based on utilization of the available liquidity, based on a pre-defined set of rules

What Drives High Yields

Yields in DeFi have been historically high on average – this is eventually what enables yield aggregation platforms such as Yearn Finance to survive and thrive. This naturally implies that utilization has been historically high, which led us to question where this demand is coming from.

There are fours potential drivers, based on the current incentive structure:

- Genuine Use Cases (real world loans)

- Demand for Governance Tokens

- Protocol Activity

- Leveraged Trading

1/ Genuine Use Cases

This use case surrounds users who either want to HODL their crypto but still need to make real life purchases, or users are currently unbanked and sidelined by the traditional financial system. There are certainly some users who fit into these categories and have used loans to make home appliance, and other, purchases.

However, we expect that these users make a marginal part of the overall borrowing demand, given high interest rates and overcollateralization requirements.

2/ Demand for Governance Tokens

Some platforms, such as Compound Finance, distribute their native token ($COMP in this case) to borrowers and lenders on a weekly basis, based on the amount they have lent / borrowed. The governance token demand argument follows that users may be incentivized to participate more in order to gain access to these tokens.

This is very unlikely to make a meaningful portion of loan demand, simply because high interest rates and overcollateralization would make it more economical to purchase these native tokens on the open market instead.

Moreover, folks looking to take advantage of this would rather participate on the lending side and earn a yield in addition to the airdrops.

3/ Protocol Activity

This argument is similar to the governance token, except for the fact that participation is incentivized by buybacks/dividends vs. airdropped tokens. Again, this is relatively unlikely to make up a meaningful part of loan demand.

4/ Leveraged Trading

This brings us to the use case that we believe is most likely. The group that is most likely to accept the high interest rates are the ones who stand to gain substantially more from the loan than the interest they pay.

One particular type of market inefficiency that these leveraged traders use DeFi loans to take advantage of is called contango. Here’s how it works:

- There exists a natural demand for crypto, specially on the long side by investors/retails

- Cheapest way to take exposure in an asset is to buy buying futures (lowest margin)

- Therefore there is a premium on future prices above spot prices (known as contango)

- Given the demand for these assets, contango is very steep

- This makes it very profitable for arbitragers to use DeFi pools to borrow crypto at a specific IRR, and then short the crypto futures, thereby locking in an arbitrage

- When future prices converge to spot, arbitragers buyback the futures and give back their crypto to realize USDT returns

This is why we will always see extremely high yields on platforms such as Aave, Maker, Compound etc. preceding a liquidation-based crash.

What Does This Means for the Future of DeFi?

One key concern this may lead to is whether DeFi is sustainable in the long run, if the main purpose it currently serves is leverage trading. How will this market evolve when volatility reduces?

It is important to understand that the overcollateralized loans leading DeFi today are not too dissimilar from gold loans (~$55B market in India alone). The only difference is that the collateralized asset is in a phase of volatile price discovery (vs. price stability). This would be similar to gold loans during the gold rush, where price was incredibly sensitivity to demand/supply shocks.

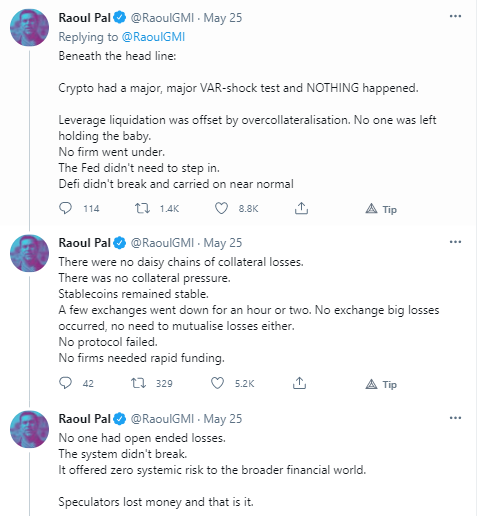

We believe that DeFi is incredibly nascent today but has the foundations to support the coming revolution. What is most promising about DeFi is that, despite the volatile activities that it currently supports, the system itself is antifragile (captured best in this tweet by Raoul Pal).

The current version of DeFi is by no means close to what the ultimate goal for the system is. However, the foundations have been set. This leads us to the question: what then, could the future of DeFi look like?

We propose four use cases that we believe could be ideal next steps in DeFi’s journey beyond its use case for trading leverage:

- Stable overcollateralized loans for real world purchases

- Undercollateralized loans for digitally identifiable assets

- Blockchain native credit score for student/healthcare loans etc.

- Consumer credit cards

1/ Stable overcollateralized loans for real world purchases

This use case will auto-materialize over time as assets such as Bitcoin and Ethereum bona fide store of value status and prices become less volatile. When this happens, speculation levels across the board will stabilize to resembles levels in traditional equity markets.

This will prompt a change in the mix of the current overcollateralized loans from trading leverage to genuine use cases, which will bring the overall interest levels down. This market will now begin looking a lot more like the gold loan market which, in India alone is ~$55B in size.

2/ Undercollateralized loans for digitally identifiable assets

As real world assets, such as homes, get blockchain native identities via NFTs, we will see a mortgage market emerge in DeFi. Customers would then be able to use either crypto assets or stablecoins to collateralize part of their loans (similar to down payments in the current mortgage market), and the NFT-d asset will back the rest of the loan.

The frictions in this market today are extremely high, making it a perfect use case for the DeFi ecosystem.

3/ Blockchain native credit score for student/healthcare loans etc.

Eventually, we expect opt-in KYC processes to allow users to build and maintain an on-chain credit score. Based on their credit scores, they may be able to lower collateral levels for certain loans such as healthcare and student loans.

This digital identity (for those who choose to build one) can then be used as the base layer to build a plethora of financial products on, much like with traditional markets. The key difference will be ease of use, speed, acceptance of and accessibility to digital assets, and most importantly trustlessness

4/ Consumer credit cards

This will be the bridge between the on-chain and real world. Customers will be able to transact and earn rewards in the form of digital assets. This use case is the most further along, being led by Gemini, Nexo Mutual and Coinbase.

Conclusion

DeFi is currently in its infancy, and a lot of the building is yet to be done. While the most prominent use case today is speculative leveraged trading on other crypto assets, we believe that the anti-fragility that has been baked into the system make it strong bedrock for a number of real world use cases that can truly disrupt the financial services sector.

Leave a Reply

Latest News

More from GCR

Featured GCR Announcement GCR Exclusive GCR Quarterly Review

GCR Market and Investment Trends ...

By Global Coin Research Team Highlights GCR is a research and investment community. As a collective, we source investments, conduct research and diligence, and make ...

The Landscape of Crypto Intents

Introduction The current blockchain paradigm requires users to devise a specific series of transactions to achieve a desired outcome. However, crafting transactions can be complicated. ...

Near AI x HZN – ...

In our last article, we outlined Near’s vision to become the hub for User-Owned AI and the steps that it is taking to develop an ...