The Current State of Undercollateralized DeFi Lending — 2021

Overview

Undercollateralized lending has been the hard-to-achieve holy grail in DeFi since as far back as 2017. Most of DeFi in its current overcollateralized form, via platforms such as Maker, Compound and Aave, serves relatively circular use cases. This is primarily because the only parties willing to post 1.5–3X leverage are traders looking to take leverage in the crypto market. Undercollateralized lending could make decentralized credit markets accessible for a wider set of use cases and potentially take DeFi mainstream.

This is why several players have been attempting to launch this market since 2017/18. The key challenge, however, has historically been finding an appropriate way to assess and assign creditworthiness of borrowers and ensure the security of lenders’ deposits. In 2020/21 the undercollateralized loan trend regained steam, and brought with is some innovative solutions to the problem of decentralized credit assessment. In this piece, we dig into each of these solutions and assess the use cases, benefits and risks of each. Overall, this space is relatively nascent and, regardless which projects / approach eventually work, undercollateralized lending will likely lead the next wave of DeFi adoption and growth.

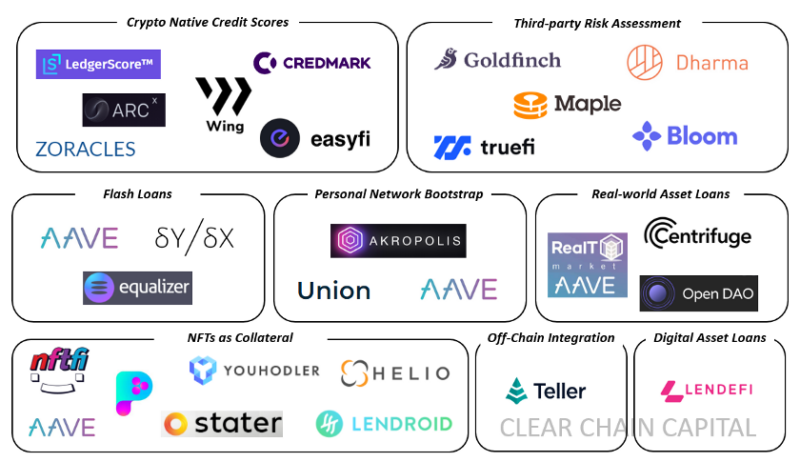

The current landscape of undercollateralized lending can be divided into eight key segments:

- Flash Loans

- Third-party Risk Assessment

- Crypto Native Credit Scores

- Off-chain Credit Integration

- Personal Network Bootstrap

- Real-world Asset Loans

- NFTs as Collateral

- Digital Asset Loans

1. Flash Loans

Use Cases: Arbitrage, collateral swap, liquidation

Advantages: Near-instant repayment, no default risk

Challenges: Cannot be used for most traditional use cases such as personal loans etc.

Flash loans are uncollateralized loans where borrowing and repayment must both occur within the same transaction. The fact that both must be complete in order for either to be processed ensures that the risk of default is essentially zero. This structure is particularly useful for arbitragers who want to exploit an opportunity between two DEXs and avoid price fluctuation, while also taking leverage. This is why >80% of the $3B+ flash loan volume has been limited to arbitrage. Overall, flash loans are an innovative product, but are unlikely to ever be used beyond arbitrage and collateral swaps.

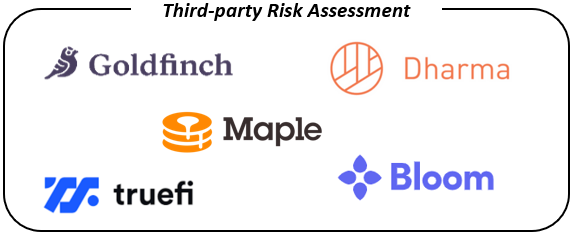

2. Third-party Risk Assessment

Use Cases: Personal loans, microfinance, decentralized prime brokerage

Advantages: Distributed counterparty risk; aligned financial incentives with credit assessors

Challenges: Bootstrapping a network of dedicated risk assessors with sufficient data + tools to make appropriate credit determinations

Third-party risk assessment has been a VC favorite in 2021, with Maple Finance and Goldfinch both raising meaningful rounds from reputable funds. This model introduces a third group, outside of lenders and borrowers, to perform the role of credit assessment . In exchange, this group must stake some of their own liquidity which will be the first to get slashed in the event of a default on a loan that they approved. This sets up a reasonable incentive structure that enables undercollateralization, while paving the way for an on-chain credit scoring system.

The key challenge with this structure will be bootstrapping a network of capable credit assessors with an appropriate level of borrower data. This is more challenging for retail outfits such as Goldfinch, than for institution-facing prime brokerage players such as Maple. However, if a platform is able to gather a capable group of assessors and make the data provisioning process smooth for borrowers, this could be a viable model.

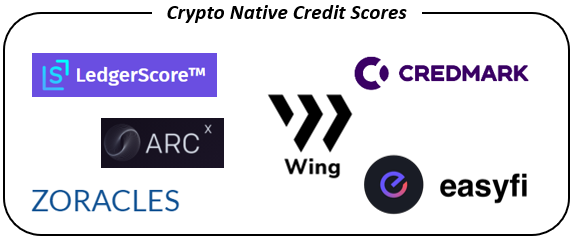

3. Crypto Native Credit Scores

Use Cases: Personal loans, microfinance etc.

Advantages: Longevity and immutability of data; cross-platform usability

Challenges: Insufficient on-chain data for most users thus far; ability of users to switch wallets if one defaults

The idea here is to bootstrap an on-chain identity by leveraging a variety of historical on-chain activity, ranging from historical loan repayment, yield farming, trading activity, governance participation etc. This could be valuable since this data will consistently compound and automatically update. Furthermore, this data could be usable across several platforms, based on user consent. While on-chain identities are likely inevitable, the initial phase that we are currently in is challenged by the ability of unlimited virtual identities and switch wallets if one defaults. The most viable solution to this will likely be some form of Zk proofs that make customers comfortable enough to share share their real world IDs on-chain and tie it to a single wallet in a pseudonymous way. Platforms that make it past this hurdle will eventually facilitate the movement of large troves data, making it relatively valuable.

4. Off-chain Credit Integration

Use Cases: Personal loans, microfinance etc.

Advantages: Sufficient data; connection to fixed identities

Challenges: Non-crypto native; dependence on TradFi infrastructure

This solution works around the bootstrapping challenges faced by crypto-native identities, by importing off-chain credit data to help underwrite undercollateralized loans. This is an appropriate strategy in the short-run, but would need to transition to harnessing on-chain, crypto-native data over time in order to plug into any decentralized stack.

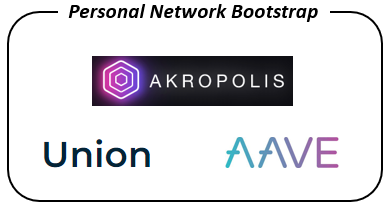

5. Personal Network Bootstrap

Use Cases: Personal loans, microfinance etc.

Advantages: Low default rate due to organic network effects

Challenges: Hard to scale if no other metrics are used; ability of users to switch wallets if one defaults

In this use case, borrowers must be approved by members of the lending pool directly. By making borrowing invite-only, the platform grows via organic network effects, introducing an element of off-chain trust. This is a clever way to bootstrap undercollateralized lending without relying on data that is likely to be limited. The key challenge around this approach will be scaling the network without incorporating additional data points, since data collection based solely on these repayments will take time to become statistically significant. Overall, this is a viable strategy that can be transformed appropriately over time to scale effectively.

6. Real World Asset Loans

Use Cases: Mortgages and other physical asset loans

Advantages: Partially collateralized by real world assets

Challenges: Potential illiquidity of physical assets, depending on market conditions

Real world assets are represented on-chain via NFTs, which collateralize another part of the loan. This looks very much like a traditional mortgage, except for the fact that loan financing is decentralized. The only challenge this approach faces is asset illiquidity, which is true even for centralized loans. While this market is very early, it is incredibly promising, given that it could eliminate a meaningful amount of red tape and bureaucracy that is characteristic of the TradFi version of real world asset loans.

7. NFTs as Collateral

Use Cases: Personal loans, microfinance etc.

Advantages: Ability to post NFTs as collateral

Challenges: Asset illiquidity

NFT-backed loans are an interesting concept that could become a niche part of the broader undercollateralized lending space. In the long-run, some NFTs could attain Jackson Pollock-like status, making the market for them relatively liquid. Since NFTs are crypto-native, expressing them on-chain and using them to settle defaults is easy if they are liquid. However, the reason that this market will likely remain a small niche in the undercollateralized lending space is that a majority of NFT artwork is likely to fall out of favor and lose market liquidity, making them a poor choice for collateral.

8. Digital Asset Loans

Use Cases: Leveraged Trading

Advantages: Control over traded asset

Challenges: Limited scale

This use case is similar to Aave, Compound etc., except for the fact that Lendefi itself maintains custody of the purchased asset in a smart contract until the loan is repaid. Therefore, if a trade on a borrowed asset is going against the borrower, the contract liquidates the position and covers the loss before returning the remaining capital. This is likely another relatively niche use case.

Conclusion

Overall it is clear that, while nascent, the undercollateralized lending space is bustling with activity. As the space continues to go through growing pains, we believe that this is likely where we will see the next wave of DeFi innovation. Eventually, the projects that adapt and survive have the potential to build the guardrails for mainstream DeFi adoption.

Leave a Reply

Latest News

More from GCR

Featured GCR Announcement GCR Exclusive GCR Quarterly Review

GCR Market and Investment Trends ...

By Global Coin Research Team Highlights GCR is a research and investment community. As a collective, we source investments, conduct research and diligence, and make ...

The Landscape of Crypto Intents

Introduction The current blockchain paradigm requires users to devise a specific series of transactions to achieve a desired outcome. However, crafting transactions can be complicated. ...

Near AI x HZN – ...

In our last article, we outlined Near’s vision to become the hub for User-Owned AI and the steps that it is taking to develop an ...